India’s cities are expanding rapidly. By 2050, nearly 50% of India’s population, about 814 million people, will be living in urban areas. That is more than the entire population of Europe! This rapid urbanisation has led to the need for massive urban infrastructure – housing, water, sanitation, waste management, energy, and transportation. Today, 62 million tons of municipal solid waste is generated in India every year. This is estimated to reach up to 165 million tons by 2030, and 436 million tons by 2050. While urban sewage generation is expected to increase by 65% by 2050, the current sewage treatment capacity stands at a mere 28%.

Municipal Corporations or Urban Local Bodies (ULBs) are the third tier of governance after Centre and State, who are primarily responsible for development and management of sustainable urban infrastructure. They are also responsible for mobilizing investment to fund this development. Institutions like the World Bank have flagged that an estimated $840 billion will be needed for urban infrastructure development in India by 2036, averaging $55 billion annually. In contrast, in 2023-24, capital expenditure by the 232 municipal corporations in India on urban infrastructure was only $29 billion, highlighting a significant funding gap. This low expenditure is because most municipal bodies in India are constrained by their limited financial resources. This limits their capacity to spend on infrastructure development, which compounds the crisis of existing as well as future urban infrastructure.

The Funding Crises of Municipal Bodies

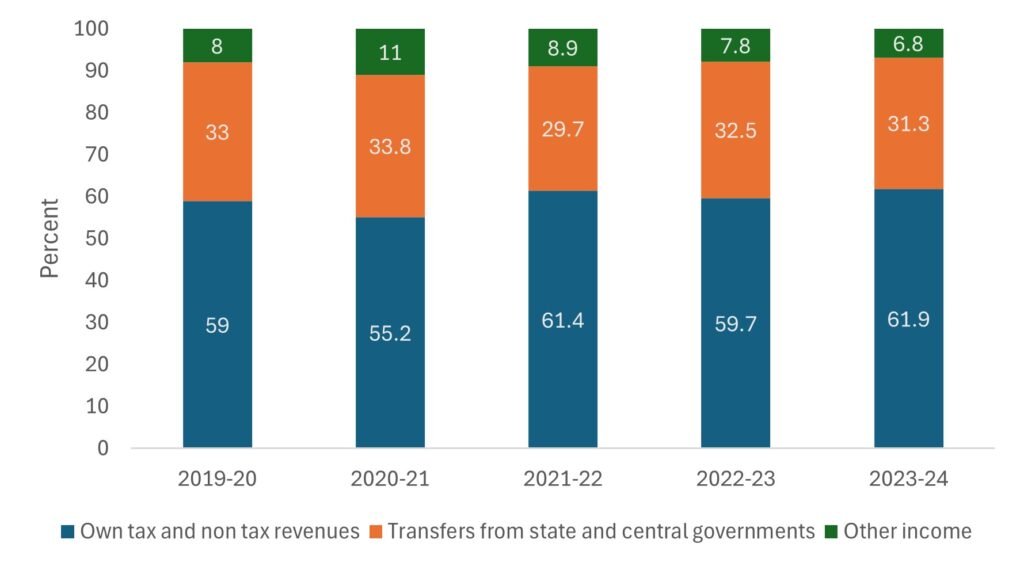

Typically, municipal bodies derive their income from Tax Revenue such as property and water taxes, State and Central government Grants and User Charges.

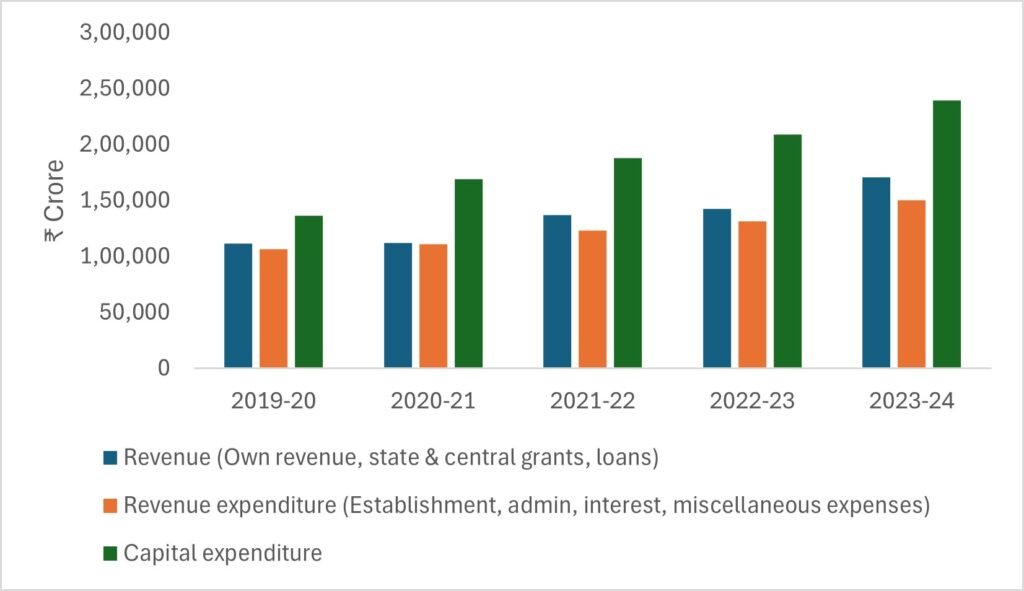

This revenue barely covers their administrative and establishment expenses for salaries and operations, leaving little for capital spending on infrastructure development. In FY 2024, total expenditure by 232 corporations including general and capital expenditure stood at ₹ 3.89 lakh crore (~ $46 billion). In contrast, at ~ $100 billion, the budget of New York City Council was more than twice the total budget of Indian ULBs (CEEW, 2025) !

The Urban Local Bodies have to depend heavily on schemes such as Smart Cities Mission, Swacch Bharat Mission and AMRUT and direct project financing by the central and state governments to plug funding gaps. Commercial financing instruments such as municipal bonds, PPPs, and loans from financial institutions accounted for only 5.2 per cent of total municipal revenue in 2023-24.

Composition of ULB Revenues

Source: RBI report on municipal finances, 2024

Source: RBI report on municipal finances, 2024

Municipal Bonds: An Untapped Financing Option for Urban Infrastructure

Raising funds through issuance of municipal bonds can be a useful mechanism for mobilizing green finance in India by ULBs and reduce their dependence on government for project financing. A municipal bond or muni bond is like a loan where a city municipal corporation raises money from investors, and repays it with interest at a fixed coupon rate over the duration of the bond. The money raised is used by the corporation to fund public infrastructure projects such as roads, buildings, water and sanitation, hospitals etc. within their city. Compared to term loans from banks, bonds with longer tenures (5-25 years) and lower interest rates at 8 – 9% coupled with GoI incentives are ideal for raising funds for public infrastructure projects which have long gestation periods.

However, the market for municipal bonds is at a very nascent stage in India.

Out of 253 municipal corporations, only 18 have issued bonds with the issuances concentrated in a select few states like Gujarat, Maharashtra, Tamil Nadu and others.

The total value of municipal bonds outstanding in India is just ₹4,204 crore (as of March 2024) which is only 0.09% of the overall corporate bond market.

The Case of Municipal Green Bonds

As India looks towards mobilising climate adaptation finance, ULBs have also started issuing green bonds for funding projects having an environmental impact such as renewable energy, water and sanitation, waste management projects. In the last decade, four municipal green bonds worth ₹694 crore have been issued for different green projects:

Ghaziabad (2021): Tertiary Water treatment plant

Ahmedabad (2023): Green energy generation

Vadodara (2024): Sewage treatment plant and drainage systems; This also happens to be India and Asia’s first certified Municipal Green Bond by Climate Bonds Initiative.

The Challenge in scaling up of Municipal Bonds

At the National Dialogue on Green Finance in Urban Local bodies: A Case for Municipal Green Bonds in India held by CEEW in New Delhi in March, I had the chance to hear experts, including those from the government, credit rating agencies, ULB officials, merchant bankers and financial institutions, deliberate upon enhancing the ecosystem for encouraging ULBs to issue municipal bonds, particularly green bonds. Key issues identified for lower issuance of muni bonds are:

Reluctance of ULBs to borrow funds as it is perceived as a sign of financial weakness.

Outdated accounting systems, poor record-keeping, and lack of proper data making risk assessments difficult for credit rating agencies.

Lack of internal financial expertise of ULB officials in accounting, capital markets, green finance, and climate adaptation projects

Small bond sizes (₹50 lakh to ₹200 crore) don’t appeal to large financial institutions and mutual funds as in terms of returns, it is not worth the risk, time and effort for them.

Irregular issuance, lack of familiarity with ULBs and long gestation period of projects lead to lack of investor trust.

Experts discuss municipal green bonds at an event convened by CEEW in Delhi.

Increasing the Adoption of Muni Bonds as a Climate Credit for Cities

The potential for municipal green bonds as estimated by CARE Ratings and World Bank is nearly $ 2.5 – 6.9 billion in the next 5-10 years, and they could become a preferred route for municipal funds due to policy and regulatory initiatives and government incentives for green projects. However, this will require:

Capacity Building of ULB officials in modern accounting systems, green finance and climate adaptation. Cities like Pimpri-Chinchwad and Vadodara are leading the way to boost credibility and attract investors with the adoption of measures such as digitization of documents and account statements, accrual based accounting systems, providing audited financial statements, and conducting third-party credit rating exercises.

Central government support: Currently the government under the AMRUT scheme is encouraging ULBs to enter the bond market by offering 13% grant per ₹100 crores worth of bonds issued. Further, regulatory frameworks have been established by The Securities & Exchange Board of India (SEBI) in 2015. To increase transparency in the municipal bond market and encourage participation of investors, the National Stock Exchange (NSE) launched India’s first Municipal Bond Index in 2023 to track the performance of municipal bonds.

Tax incentives to attract retail investors

Regular bond issuances to build investor confidence

Municipal bonds, especially green bonds, could be a mechanism for India’s cities to raise climate finance. In the face of rising urban population and its expanding needs, and climate related disasters, they offer a way to fund crucial infrastructure, boost climate resilience, and reduce dependence on government grants. Scaling up will require capable leadership in ULBs who can adopt modern administrative and financial discipline, investor friendly policies, and more risk taking by large investors. The future of India’s cities depends on how well we finance them, and municipal bonds could be major green bricks for building them.

Sources :

RBI Report on Municipal Finances, 2024.

Bibhudatta, Amlan and Dishant Rathee. 2025. Unlocking Green Finance for India’s Urban Local Bodies through Municipal Green Bonds. New Delhi: Council on Energy, Environment and Water

Circular Economy in Municipal Solid and Liquid Waste, MoHUA

https://www.worldbank.org/en/news/opinion/2024/01/30/gearing-up-for-india-s-rapid-urban-transformationhttps://www.moneycontrol.com/news/opinion/revamping-urban-local-bodies-addressing-financial-and-governance-challenges-12882456.html

Saurabh contributes to the research and communication efforts in the water sector at Sankala. He holds a bachelor’s degree in chemistry from St. Stephen’s College, Delhi and master’s degrees in chemistry from IIT Roorkee and chemical engineering from University of Twente, Netherlands where he studied on a full scholarship from Royal Dutch Shell. He has diverse experience in project implementation and management, research, engineering, and consulting in the environment sector.

He led the implementation, techno-commercial management, monitoring, and evaluation of two pilot projects with Municipal Corporation of Delhi on decentralized waste management and urban drain desilting. He also has extensive experience in engineering and consulting on water, sewage and industrial effluent treatment projects, techno-commercial studies, science communication, onboarding of partners and technical experts, vendor and contract management, program budget management and organising events, roundtables.